Source: Institute for Supply Management – September 2, 2020

Economic activity in the manufacturing sector grew in August, with the overall economy notching a fourth consecutive month of growth, say the nation’s supply executives in the latest Manufacturing ISM® Report On Business®.

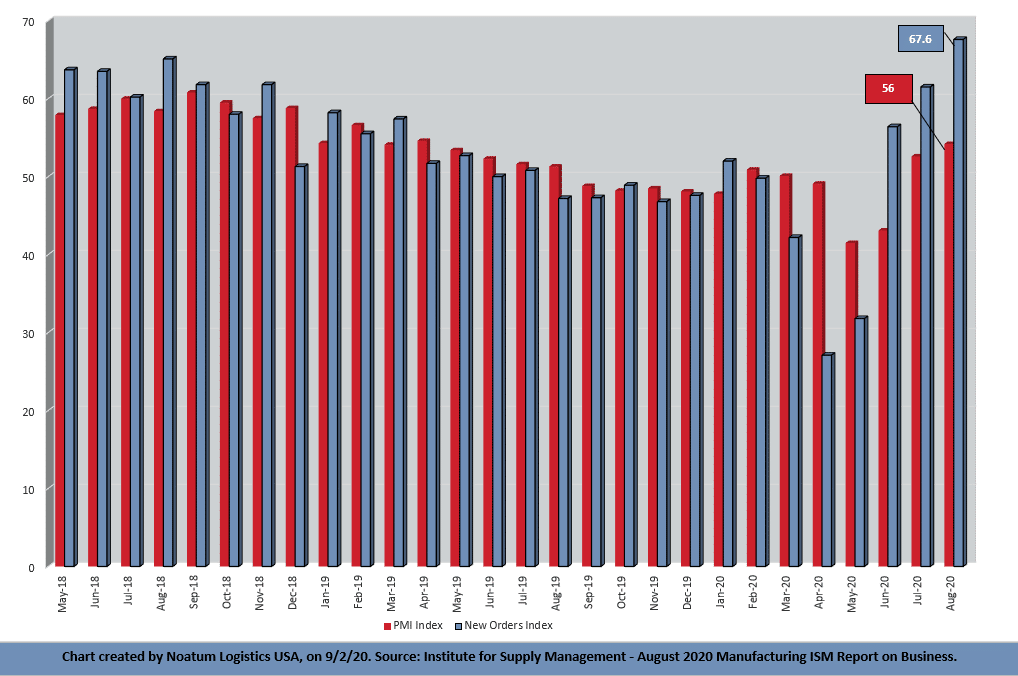

The report was issued today by Timothy R. Fiore, CPSM, C.P.M., Chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee: “The August PMI® registered 56 percent, up 1.8 percentage points from the July reading of 54.2 percent. This figure indicates expansion in the overall economy for the fourth month in a row after a contraction in April, which ended a period of 131 consecutive months of growth. The New Orders Index registered 67.6 percent, an increase of 6.1 percentage points from the July reading of 61.5 percent. The Production Index registered 63.3 percent, up 1.2 percentage points compared to the July reading of 62.1 percent. The Backlog of Orders Index registered 54.6 percent, an increase of 2.8 percentage points compared to the July reading of 51.8 percent. The Employment Index registered 46.4 percent, an increase of 2.1 percentage points from the July reading of 44.3 percent. The Supplier Deliveries Index registered 58.2 percent, up 2.4 percentage points from the July figure of 55.8 percent.

“The Inventories Index registered 44.4 percent, 2.6 percentage points lower than the July reading of 47 percent. The Prices Index registered 59.5 percent, up 6.3 percentage points compared to the July reading of 53.2 percent. The New Export Orders Index registered 53.3 percent, an increase of 2.9 percentage points compared to the July reading of 50.4 percent. The Imports Index registered 55.6 percent, a 2.5-percentage point increase from the July reading of 53.1 percent.

“After the coronavirus (COVID-19) brought manufacturing activity to historic lows, the sector continued its recovery in August, the first full month of operations after supply chains restarted and adjustments were made for employees to return to work. Survey Committee members reported that their companies and suppliers operated in reconfigured factories, with limited labor application due to safety restrictions. Panel sentiment was generally optimistic (1.4 positive comments for every cautious comment), though to a lesser degree compared to July. Demand expanded, with the (1) New Orders Index growing at very strong levels, supported by the New Export Orders Index expanding modestly; (2) Customers’ Inventories Index at its lowest figure since June 2010, a level considered a positive for future production, and (3) Backlog of Orders Index indicating growth for the second consecutive month. Consumption (measured by the Production and Employment indexes) contributed positively (a combined 3.3-percentage point increase) to the PMI® calculation, with industries continuing to expand output compared to July. Inputs — expressed as supplier deliveries, inventories and imports — were flat during the survey period, due to supplier delivery issues returning and import levels expanding moderately. Inventory levels contracted again due to strong production output and supplier delivery difficulties. Inputs likely were the biggest impediment to production growth and contributed negatively (a combined 0.2-percentage point decrease) to the PMI® calculation. (The Supplier Deliveries and Inventories indexes directly factor into the PMI®; the Imports Index does not.) Prices continued to expand and at higher rates, reflecting a shift to seller pricing power — a positive for new-order growth.

“Demand and consumption continued to drive expansion growth, with inputs representing near- and moderate-term supply chain difficulties. Among the six biggest manufacturing industries, Food, Beverage & Tobacco Products remains the best-performing sector, with Chemical Products; Computer & Electronic Products; and Fabricated Metal Products growing strongly. Transportation Equipment also expanded, but at a low rate. Petroleum & Coal Products sunk into contraction territory.

“Impacted by the current economic environment, many panelists’ companies are holding off on capital investments for the rest of 2020. In addition, (1) commercial aerospace equipment companies, (2) office furniture and commercial office building subsuppliers and (3) companies operating in the oil and gas markets — as well as their supporting supply bases — are and will continue to be impacted due to low demand. These companies represent approximately 20 percent of manufacturing output. This situation will likely continue at least through the end of the year,” says Fiore.

Of the 18 manufacturing industries, 15 reported growth in August, in the following order: Wood Products; Plastics & Rubber Products; Food, Beverage & Tobacco Products; Textile Mills; Chemical Products; Computer & Electronic Products; Primary Metals; Fabricated Metal Products; Machinery; Apparel, Leather & Allied Products; Nonmetallic Mineral Products; Miscellaneous Manufacturing; Electrical Equipment, Appliances & Components; Paper Products; and Transportation Equipment. The three industries reporting contraction in August are: Printing & Related Support Activities; Petroleum & Coal Products; and Furniture & Related Products.

Click here to access the entire release from the Institute for Supply Management website.