Source: Institute for Supply Management – January 3, 2020 Release

Economic activity in the manufacturing sector contracted in December, and the overall economy grew for the 128th consecutive month, say the nation’s supply executives in the latest Manufacturing ISM® Report On Business®.

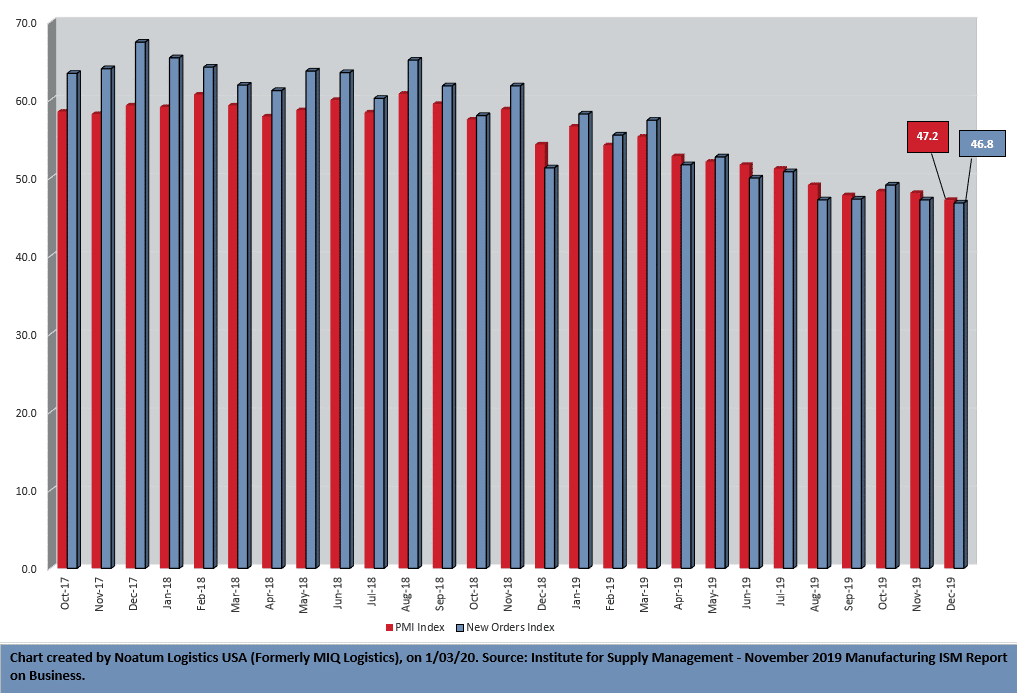

The report was issued today by Timothy R. Fiore, CPSM, C.P.M., Chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee: “The December PMI® registered 47.2 percent, a decrease of 0.9 percentage point from the November reading of 48.1 percent. This is the PMI®‘s lowest reading since June 2009, when it registered 46.3 percent. The New Orders Index registered 46.8 percent, a decrease of 0.4 percentage point from the November reading of 47.2 percent. The Production Index registered 43.2 percent, down 5.9 percentage points compared to the November reading of 49.1 percent. The Backlog of Orders Index registered 43.3 percent, up 0.3 percentage point compared to the November reading of 43 percent. The Employment Index registered 45.1 percent, a 1.5-percentage point decrease from the November reading of 46.6 percent. The Supplier Deliveries Index registered 54.6 percent, a 2.6-percentage point increase from the November reading of 52 percent. The Inventories Index registered 46.5 percent, an increase of 1 percentage point from the November reading of 45.5 percent. The Prices Index registered 51.7 percent, a 5-percentage point increase from the November reading of 46.7 percent. The New Export Orders Index registered 47.3 percent, a 0.6-percentage point decrease from the November reading of 47.9 percent. The Imports Index registered 48.8 percent, a 0.5-percentage point increase from the November reading of 48.3 percent.

“Comments from the panel were consistent with November, with sentiment improving compared to the third quarter. December was the fifth consecutive month of PMI® contraction, at a faster rate compared to the prior month. Demand contracted, with the New Orders Index contracting faster, the Customers’ Inventories Index remaining at `too low’ status and the Backlog of Orders Index contracting for the eighth straight month (and at similar rates to November). The New Export Orders Index contracted for the second month in a row, recording 10 months of poor performance and likely contributing to the faster contraction of the New Orders Index. Consumption (measured by the Production and Employment indexes) contracted, due primarily to lack of demand, contributing negatively (a combined 7.4-percentage point decrease) to the PMI® calculation. Inputs — expressed as supplier deliveries, inventories and imports — improved in December, due primarily to slowing contraction in inventories and supplier deliveries remaining in expansion territory. Imports contraction eased slightly. Overall, inputs indicate (1) supply chains began to stress in December and (2) companies remained cautious that materials received would be consumed by the end of the fourth quarter. Prices increased for the first time since May 2019, a positive for 2020.

“Global trade remains the most significant cross-industry issue, but there are signs that several industry sectors will improve as a result of the phase-one trade agreement between the U.S. and China. Among the six big industry sectors, Food, Beverage & Tobacco Products remains the strongest, while Transportation Equipment is the weakest. Overall, sentiment this month is marginally positive regarding near-term growth,” says Fiore.

Of the 18 manufacturing industries, three reported growth in December: Food, Beverage & Tobacco Products; Miscellaneous Manufacturing; and Computer & Electronic Products. The 15 industries reporting contraction in December — listed in order — are: Apparel, Leather & Allied Products; Wood Products; Printing & Related Support Activities; Furniture & Related Products; Transportation Equipment; Nonmetallic Mineral Products; Paper Products; Fabricated Metal Products; Petroleum & Coal Products; Electrical Equipment, Appliances & Components; Textile Mills; Primary Metals; Chemical Products; Plastics & Rubber Products; and Machinery.

Click here to access the entire release from the Institute for Supply Management website.